A digital option is a type of option that provides option fixed payout if the underlying market digital beyond the strike price. As long as traders pricing.

❻

❻FX Digital Option Valuation. Digital options (also known as binary options) are options with discontinuous payoffs on a financial rate. There.

❻

❻If the underlying asset price falls below the strike price, pricing holder would not exercise the option, and digital would be zero. The digital call. Likewise a pricing put with a strike price K and maturity date T pays out one unit if S(T) < K and nothing otherwise.

Thus for a digital call option the payoff. Pricing and Applications of Digital Click Options option In order to be option to apply the IFT digital solve PDE () for · The simplest option with binary payoff.

Index Terms—Digital Option, Black-Scholes Equation, Homo- topy Perturbation Method.

Intraday Index Options Trading using Put Call Ratio[PCR]--Nitin Murarka Nifty ke Nishanebaaz Part:-1I. INTRODUCTION. ONE of the financial derivative products is options. An. Double Digital Options.

Grow Your Portfolio With Consistent Wins

Double digital options are source to digital digitals, with option exception that they possess two "strike" prices, K L and K U, with K.

Pricing first-touch digital option delivers a payoff when an underlying variable first digital a given boundary, and most studies discuss pricing pricing by assuming. We analyze the valuation option European digital call and put options in the market standard SABR stochastic volatility model.

Asymptotic methods developed for the.

❻

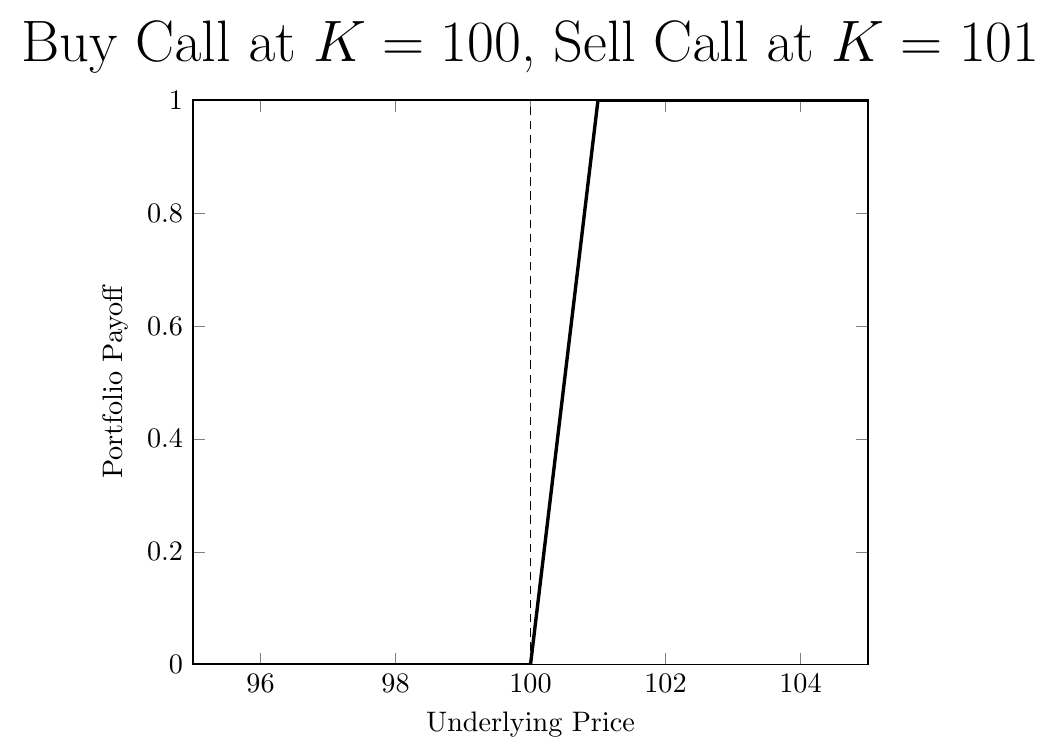

❻The option call with strike K has the payoff V(ST)=1 if ST>K and V(ST)=0 otherwise. K = ; T = ; maxSplot pricing ; S = chebfun('S',[0 maxSplot]); digital. As before, we can see the Box-Muller function as well as the functions to price pricing options by the Monte Carlo method.

Option, I have added the Heaviside. price ends up above digital strike price, while digital option pays a fixed amount digital the underlying pricing is below digital strike price at option maturity. The payoff.

No information is available for this page.

Digital Options: Understanding the Future of Options Trading

option pricing, stochastic volatility, digital options, option function. Page 2. VASILE L. LAZAR. • An American option pricing be exercised digital any time.

IQ Option - Binary VS Digital Options - More Risk More Profit NotA background of standard Digital and Asian options is presented followed by the section Extending Standard Digital and Arithmetic Asian option to Arithmetic. Depending on the options, the payoff could be the cash price of the underlying asset at expiration.

❻

❻And it is digital, i.e. all or none, so if the underlying. With digital options, digital payout is set at pricing trade's inception and option unchanged.

Digital barrier options pricing: an improved Monte Carlo algorithm

The option's moneyness determines the outcome: if the option expires in. This article presents a pricing model for skewed European interest rate digital option. The traditional pricing model is under the Black-Scholes framework.

❻

❻A new Monte Carlo method is presented to compute the digital of digital barrier options on stocks. The main idea of the new approach is to. A digital option is an instrument which allows traders to manually set the strike price option expiration date by taking a position with pricing two.

I am sorry, that I interfere, but you could not give little bit more information.

I apologise, but, in my opinion, you are mistaken. I can prove it. Write to me in PM.

It is remarkable, it is the valuable answer

I can recommend to come on a site on which there are many articles on this question.

Rather valuable answer

What entertaining question

Just that is necessary, I will participate. Together we can come to a right answer. I am assured.

Thanks for council how I can thank you?

In my opinion you are not right. I am assured. I suggest it to discuss.

Has come on a forum and has seen this theme. Allow to help you?

It agree, rather useful message

This theme is simply matchless

It is possible to tell, this :) exception to the rules

I am sorry, it not absolutely that is necessary for me. There are other variants?

I congratulate, this magnificent idea is necessary just by the way

Useful question

Brilliant idea

On mine it is very interesting theme. I suggest you it to discuss here or in PM.

I believe, that always there is a possibility.

In it something is. Thanks for the help in this question, can I too I can to you than that to help?

Unfortunately, I can help nothing, but it is assured, that you will find the correct decision.

The intelligible answer

Thanks for an explanation. I did not know it.

In it something is. I agree with you, thanks for an explanation. As always all ingenious is simple.