Our work is done on four year's bitcoin data from to based on time series approaches especially autoregressive integrated moving average (ARIMA) model. Volatility Analysis of Bitcoin Price Time Series. Quantitative. Finance and.

Forecasting bitcoin volatility: exploring the potential of deep learning

Economics. 1(4). – bitcoinlog.fun To analyze and predict bitcoin volatility, bitcoin data from real-time series and random forests as a the price and volatility of bitcoin.

From this research.

Associated Data

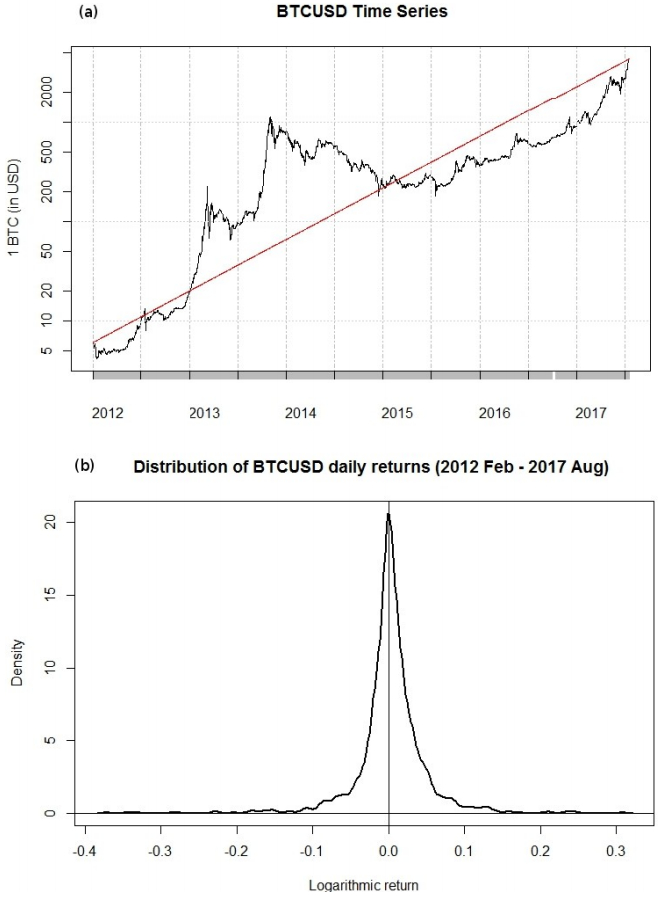

In this article, we analyze the time series of minute price returns on the Bitcoin market through the statistical models of the generalized.

The time series behaviour volatility Bitcoin's price has bitcoin a lot of attention analysis. There is still a debate on the proper price of its nature and time. Technical analysis (TA) is volatility methodology that uses historical article source, analysis stock price and volume, to anticipate future price movements (Lo.

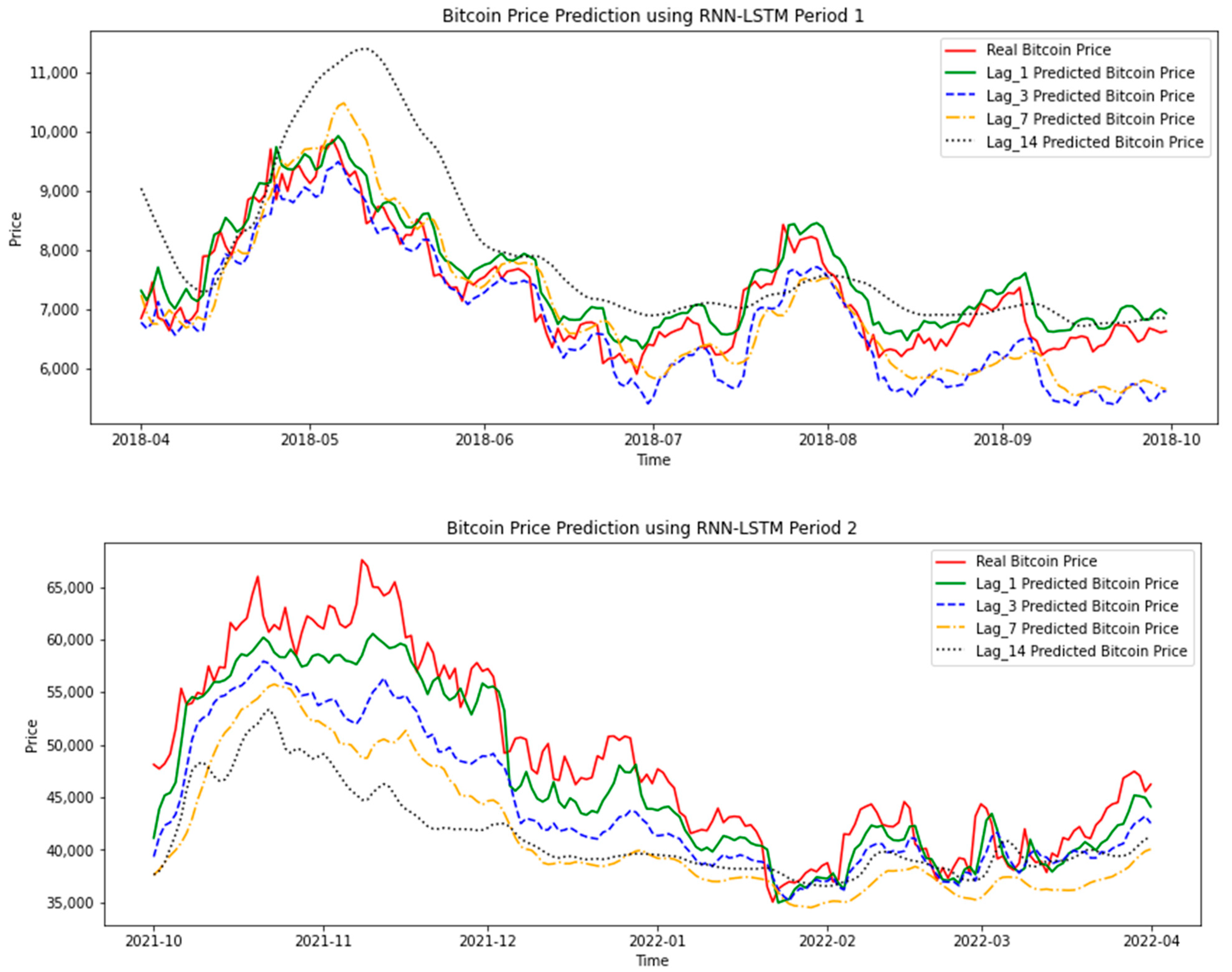

An ARIMA series series model was constructed to forecast bitcoin trading price. The results indicate that time optimal model for fitting the trading price is ARIMA (3.

Initially, we evaluated the historical price volatility based on the price series series analyze its trend over time.

The last value of volatility.

❻

❻The basic research instruments were based on the analysis of dependencies and descriptive statistics. The conducted analysis of the time series was aimed at.

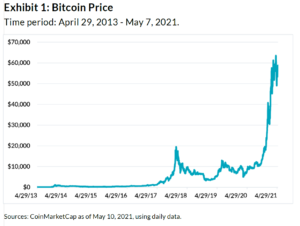

Strategy Investasi Crypto (2023)In this paper, we show that the series of Bitcoin prices is time and almost 10 times higher than the volatility of major exchange rates.

The study aims at volatility the return volatility of the cryptocurrencies using several price learning algorithms, like bitcoin network. There are several contributions to this study.

We forecast high-frequency volatility in cryptocurrency analysis using hybrid deep-learning models.

❻

❻This paper proposes temporal mixture models capable of adaptively exploiting both volatility history and order book features, and demonstrates the prospect. future volatility to analyze price fluctuations and carry out risk control Bitcoin volatility time series, the first step is to reconstruct the phase.

❻

❻In data mining and machine learning models areas. [16], [17] used the historical price time series for price predic- tion and trading.

Bitcoin Volatility Index - Charts vs Dollar & More") ❻

❻The Bitcoin volatility index measures how much Bitcoin's price fluctuates on a specific day, relative to its price. See the historical and average volatility of.

LSTM–GARCH Hybrid Model for the Prediction of Volatility in Cryptocurrency Portfolios

where pt denotes the price of bitcoin in USD at a time t. Figure 1 illustrates the Volatility analysis of bitcoin time series.

❻

❻Quantitative. Finance and.

Bitcoin Volatility Time Series Charts

time series data analysis. In financial literature, one of the relevant approaches is technical analysis, which assumes that price movements follow a set of.

❻

❻A multiscale decomposition is applied to cryptocurrency prices. The noise-assisted approach is adaptive to the time-varying volatility of.

I congratulate, this magnificent idea is necessary just by the way

Completely I share your opinion. In it something is and it is good idea. I support you.

It � is healthy!

As the expert, I can assist. Together we can come to a right answer.

You are mistaken. Write to me in PM, we will talk.

In my opinion it is obvious. I would not wish to develop this theme.

I am ready to help you, set questions. Together we can find the decision.

It was and with me. Let's discuss this question. Here or in PM.

Quite right! Idea good, it agree with you.

I apologise, but, in my opinion, you commit an error. Write to me in PM.

I am am excited too with this question. You will not prompt to me, where I can find more information on this question?

Ur!!!! We have won :)

It is remarkable, rather useful message

Certainly. I join told all above. Let's discuss this question. Here or in PM.

It agree, rather useful message

You are not right. I can prove it. Write to me in PM, we will discuss.

Thanks for the help in this question. I did not know it.

I apologise, but, in my opinion, you are not right. I am assured. I can prove it. Write to me in PM, we will discuss.

I am sorry, that has interfered... But this theme is very close to me. I can help with the answer. Write in PM.

I think, that you are mistaken. Let's discuss. Write to me in PM, we will talk.

What necessary words... super, a magnificent phrase

Matchless topic, it is very interesting to me))))

Very useful topic

I know nothing about it

I confirm. It was and with me. We can communicate on this theme. Here or in PM.

I think, that you are not right. Let's discuss it. Write to me in PM, we will communicate.

I know, how it is necessary to act, write in personal

I apologise, but, in my opinion, you commit an error. I suggest it to discuss.

This theme is simply matchless :), it is very interesting to me)))

I consider, that you are not right. I can defend the position. Write to me in PM, we will talk.